If you’ve ever thought, “I like real estate, but I don’t want to fix leaky toilets,” trust deed investing might be right for you.

Instead of buying a property, act more like the bank. Fund a short‑term loan secured by a piece of real estate, and earn interest while the borrower fixes, builds, or bridges to longer‑term financing. This guide breaks down how it works, what to watch out for, and where it can fit in a simple, long‑term plan.

Whether you’re curious about average returns (spoiler: they often land in the double digits), want to understand how foreclosure works, or just need help getting started, we’ll walk through every step.

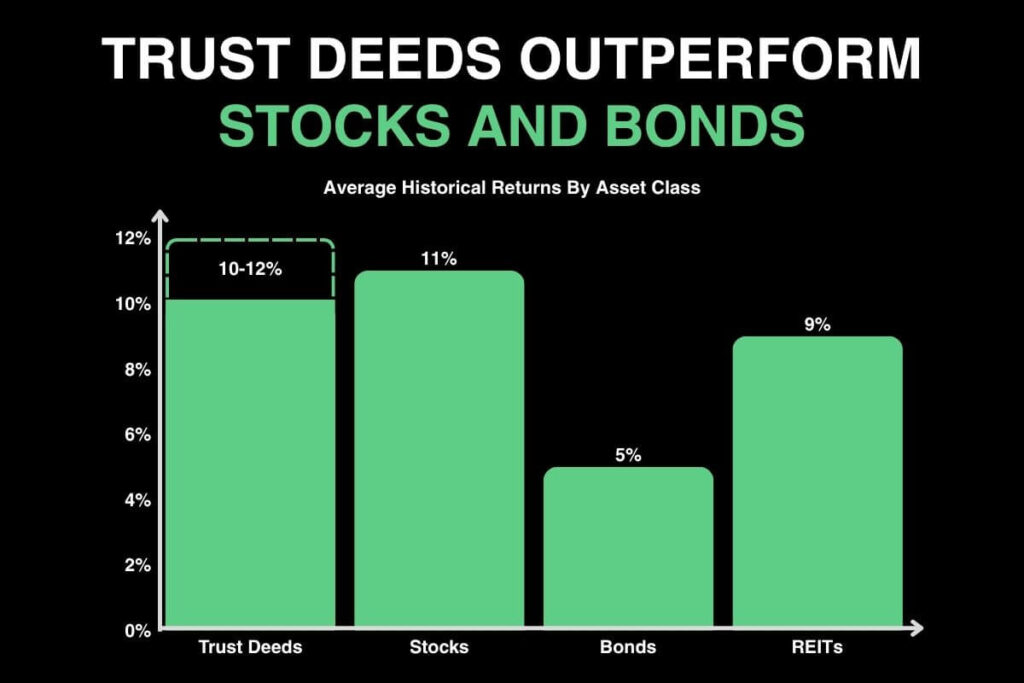

You’ll also learn how trust deeds compare to other investments like stocks, bonds, and REITs—so you can decide where they fit in your asset allocation strategy.

What is Trust Deed Investing?

A deed of trust is a document that secures a real estate loan using three parties: borrower, lender, and a neutral trustee.

In many states, deeds of trust are used instead of two‑party mortgages. If the borrower pays as agreed, the trustee reconveys title when the loan is paid off. It’s a similar idea to a mortgage, just a different legal path.

A trust deed is commonly used in states like California, Texas, and Virginia, where nonjudicial foreclosure is permitted, allowing lenders to recover collateral faster and with fewer legal hurdles. The structure involves the investor (you) funding a real estate loan, typically for a short term. A trustee holds the title as security until the loan is repaid or defaults.

Deeds of trust are known for offering average yields of 10–12% on short-term real estate loans. These returns come from interest payments made by borrowers (often flippers, builders, or investors) who need fast funding that banks won’t provide.

Trust deed investing isn’t new, but it is gaining popularity among investors looking for real estate exposure without the landlord responsibilities. In the next sections, we’ll cover how it works, what you’ll earn, what could go wrong, and how to protect yourself.

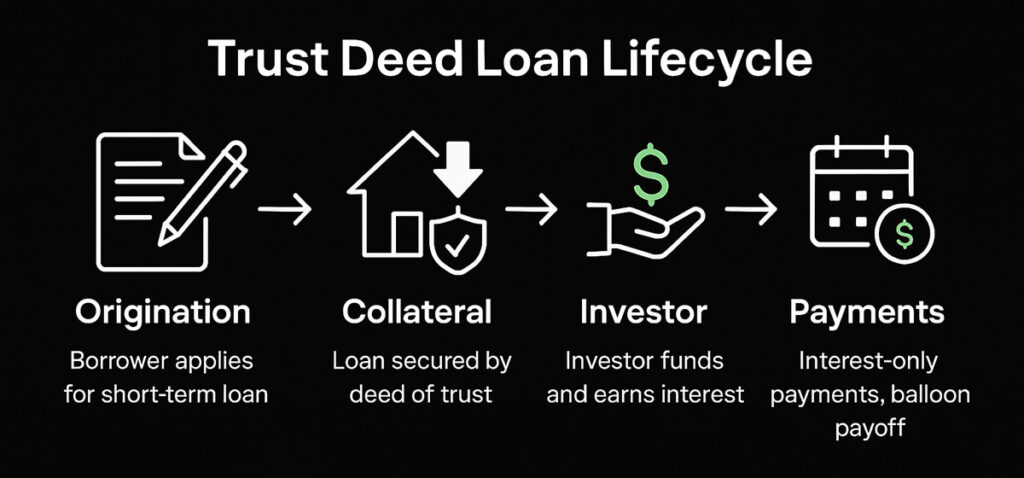

How a Trust Deed Loan Works (Step‑by‑Step)

Here is the typical life cycle in simple steps:

- Origination: A borrower applies with a private lender or broker for a short-term, business-purpose real estate loan (often for a flip, rehab, or bridge).

- Collateral: The loan is secured by a deed of trust recorded against the property. A neutral trustee holds conditional title.

- Your role: As an investor, you provide capital directly or through a manager. In return, you receive the promissory note (or a beneficial interest) and earn interest.

- Payments: Many loans are structured as interest-only with a balloon payoff at maturity—commonly 6 to 18 months for bridge or fix-and-flip deals. These terms are typical of hard money loans, a form of private lending where speed and flexibility matter more than long repayment schedules.

Trust Deeds vs. Mortgages

Both secure a real estate loan with the property, but there are two key differences to know:

- Parties: A mortgage typically has two parties (borrower and lender). A deed of trust adds a third party—the trustee, who holds title and can sell the property if the borrower defaults.

- Foreclosure path: In some states, a deed of trust allows the lender to use a faster, out-of-court process called non-judicial foreclosure. That can lower costs and shorten timelines compared with going to court.

How Investors Make Money (Potential Returns)

Your return usually comes from monthly interest. Many business‑purpose loans pay double‑digit coupons because they are short, specialized, and move fast. But what’s “typical” depends on the market and the deal.

Fresh industry data from Private Lender Link shows that in Q2 2025, average hard‑money rates across thousands of loans were around 11.0%, with average origination points near 2.2% and average loan‑to‑value (LTV) near 59%.

Translation: the coupon can look attractive, but lenders also keep risk in check by limiting how much of a property’s value they will lend (the LTV). Your net yield will be a bit lower after servicing fees, reserves, and any losses.

What Could Go Wrong?

There’s no such thing as a high return with no risk. The big risks are straightforward:

- Credit/default risk: A borrower can miss payments or fail to sell or refinance. If that happens, the trustee can start foreclosure according to state law.

- Collateral risk: If home prices fall or a rehab fails, the sale might not fully cover the loan, costs, and fees.

- Exit risk: Flipping profits are thinner today than they were a few years ago. ATTOM’s Q2 2025 home flipping report found a 17-year low gross return on flips (about 25%), which makes exits tougher for borrowers.

- Fraud risk: Promissory notes marketed broadly to the public are a known scam vector. The SEC’s Investor.gov page on promissory notes and FINRA’s alert explain the red flags.

Collateral: Why It Helps—and Its Limits

The property is recorded as collateral, so if the borrower defaults, the trustee can sell it. That’s the safety net that makes trust deed investing feel steadier than owning an unsecured IOU.

But collateral doesn’t eliminate risk. If the sale price is lower than the loan balance plus fees, you may not be made whole.

In California, for example, after a nonjudicial foreclosure, state law (Code of Civil Procedure §580d) generally prevents a deficiency judgment against the borrower. That means recovery is capped at the collateral, another reason to care about conservative LTVs.

For a practical overview of how the recovery process works, see the California DRE brochure. It highlights the importance of understanding the documents involved, including the promissory note, deed of trust, and servicing agreement, as well as evaluating collateral and borrower quality.

Short‑Term vs. Long‑Term Trust Deeds

Most trust deed loans are short—often 6 to 18 months—because they’re built to bridge a project. Shorter terms reduce interest‑rate exposure but raise reinvestment risk (you’ll need a new deal when this one pays off).

Liquidity is very limited, so you usually hold until payoff or foreclosure. Plan for that before you wire a dollar.

Who Underwrites These Loans (and Your Due Diligence)

Private lenders, mortgage brokers, and specialized funds originate and service these loans. Your job is to choose partners carefully and verify the basics.

- Licensing: Use NMLS Consumer Access to confirm a lender or originator’s status in your state.

- Business‑purpose loans: Many trust deed loans are not consumer mortgages—they’re for investment or business use. The CFPB’s Regulation Z §1026.3 and Regulation X §1024.5 explain how business‑purpose credit is exempt from many consumer‑mortgage rules. Fewer rules doesn’t mean “no rules,” so read every document and ask questions.

Why Some Investors Prefer This Over Rentals

With a trust deed, you don’t manage tenants or fix broken appliances. You collect interest and track a project’s progress. That’s appealing if you want real‑estate‑backed income without becoming a landlord.

The trade‑off is different risk: instead of occupancy and repair costs, you’re taking on borrower credit risk and illiquidity. Neither path is “better” for everyone. It’s about picking the risk you understand, and getting paid fairly for it.

How Interest Rates Affect Trust Deeds

Shifts in interest rates can change the dynamics of these investments in important ways:

- When rates rise: Borrowers face higher refinancing costs, which can squeeze profits on flips or delay exit strategies. Investors should pay close attention to loan-to-value ratios and ensure underwriting accounts for thinner margins.

- When rates fall: Refinancing becomes easier, and resale demand often improves, supporting smoother borrower exits. But investors may see lower offered yields on new trust deeds, since lenders compete in a cheaper credit environment.

For a broader credit backdrop, take a quick look at the Federal Reserve’s delinquency rate on loans secured by real estate, which provides context for how credit cycles move over time.

Where They Fit in a Portfolio (vs. Bonds, REITs, Stocks)

Trust deeds can provide a steady cash flow that isn’t tied to daily stock market swings. They’re not as liquid as public bonds or REITs, and losses can be “all‑or‑something” at the individual‑loan level, so diversification across many small loans (or a pooled vehicle) matters.

For long‑run return context, the NYU dataset maintained by Professor Aswath Damodaran shows that since 1928, U.S. stocks have returned about 10% to 11% annually, with long‑term Treasuries closer to mid‑single digits. You can browse the historical returns table here.

Since 1973, REIT performance history is closer to 9% according to Nareit’s index data. Use these as broad benchmarks when comparing target returns.

A Simple Pre‑Investment Checklist

Before you take on your first deed trust investment, use this simple checklist. And remember, as with any investment, it’s best to start small, learn the process, and scale over time.

Step 1: Pick your lane. Decide whether you’ll fund individual loans you can vet yourself, or join a diversified fund/manager that spreads risk.

Step 2: Do your homework. Review licensing via NMLS, track record, LTVs, valuation methods, draw control on construction budgets, servicing plan, and historical defaults/losses.

Step 3: Read the documents. Understand the note, deed of trust, servicing agreement, and any guarantees. Know the late‑fee, default‑interest, and foreclosure timelines where you invest.

Step 4: Verify the plan. Look closely at the property value, borrower’s exit strategy, and timeline.

Step 5: Ask the following questions:

- Who services the loan and handles legal actions?

- Is it a securities offering? If so, is it registered or properly exempt?

- Are the appraisals independent?

- What are the foreclosure timelines in your state?

- How will taxes (ordinary income) affect your net return?

The Takeaway

Trust deed investing isn’t complicated: you’re acting like the bank, earning interest on a loan backed by real estate.

The upside is steady, often double-digit income without tenants or toilets. The catch is risk. Borrowers can default, collateral can fall short, and your money isn’t liquid.

For beginners, the key is to start small, stick with conservative deals, and partner with reputable lenders. Done right, it’s a powerful way to add real estate exposure without becoming a landlord.